Knowing your costs (well) to sell better

Many entrepreneurs complain that they don't earn enough or that they can't calculate their selling prices correctly. In reality, the problem is that they don't know how to allocate costs to the product.

Accountants often lack the time—or specific skills—to set up an industrial costing system that can determine sales price lists based on objective data.

Thus, too often, prices are set “by feel,” with rough estimates or hypothetical margins.

The result? Products sold below cost, eroded margins, and decisions made in the dark.

The limitation of SMEs: the lack of industrial accounting

Most SMEs do not have an analytical industrial accounting system capable of providing reliable information on production costs and contribution margins for each individual order or product line.

But the good news is that there is a simple and sustainable alternative, even for small and medium-sized businesses: industrial profit and loss analysis, integrated with a mapping of the organizational and production structure.

This approach allows you to clearly identify direct and indirect costs, and to calculate the hourly rates and specific costs to apply to the bills of materials – the true “recipes” for each product. Only in this way is it possible to define sales prices that are consistent with actual company costs and margin objectives.

The Direct Costing Method: The Most Effective Way

The most effective methodology for determining industrial costs is Direct Costing.

This method attributes direct variable costs (raw materials, direct labor) to the product, but also takes into account all specific production costs of a fixed or semi-fixed nature, such as:

- depreciation of “new” machinery;

- electrical energy absorption;

- indirect labor;

- consumables;

- maintenance and technical services.

The goal is to build a realistic sales quote model that takes every variable into account and allows the entrepreneur to sell at the right price, protecting margins and competitiveness.

When a leap in quality is needed: the ESM

For companies looking to go further, the solution is to implement a Manufacturing Execution System (MES). This is advanced management software that, in addition to scheduling production and managing inventory, tracks actual production quantities and times, allowing for continuous comparison with the theoretical data in the bill of materials.

This approach allows you to understand where income is generated, where it is lost, and how to improve it.

For SMEs that do not want to incur the costs of a complete MES, it is possible to adopt simpler software interfaces, capable of automatically collecting production times and quantities directly from the machines.

Profitability analysis by processing phases

Let's take a concrete example: a company that processes stainless steel to order wants to know the profitability of its products in order to set more accurate selling prices.

There are two approaches: 1️⃣ Analyze revenues and costs for each individual job; 2️⃣ Or analyze revenues and costs by production phase.

For companies with many orders, the second option is more efficient: it allows you to set up analysis by cost center and production phase, avoiding the complexity of job-by-job accounting.

By determining average hourly production costs and collecting real data from machines (via MES or interface), it is possible to compare actual times with theoretical ones.

This way, the industrial cost per unit of measurement (€/m2, €/Kg, etc.) is obtained, which can be compared with the sales price lists and the profitability of each process verified.

From data to margin: control and decision

Thanks to this methodology, each process can be associated with the relevant customer, allowing for a profitability analysis by machine, by phase, and by customer.

An approach typical of Make to Order (MTO) systems, perfect for companies that work to order.

In this way, the entrepreneur has a complete and up-to-date overview:

- knows how much it costs to produce each item;

- knows the real margins of each process;

- can make quick, numbers-based decisions.

Because true industrial management control isn't done after the fact: it's built, day after day, on actual production data.

Let's now look at some concrete examples of commercial estimates that we have created for companies such as:

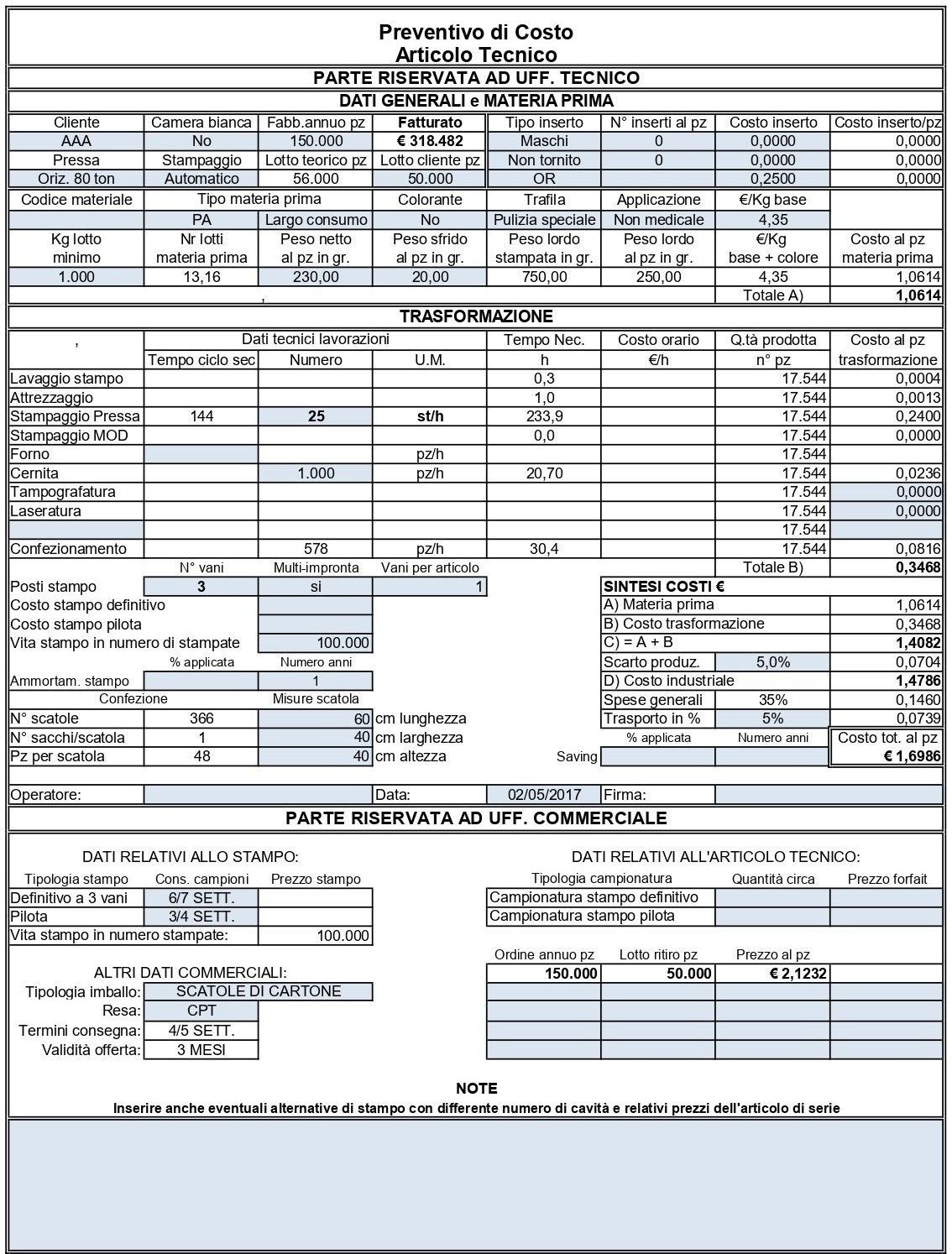

1) molding of technical plastic articles, made to order;

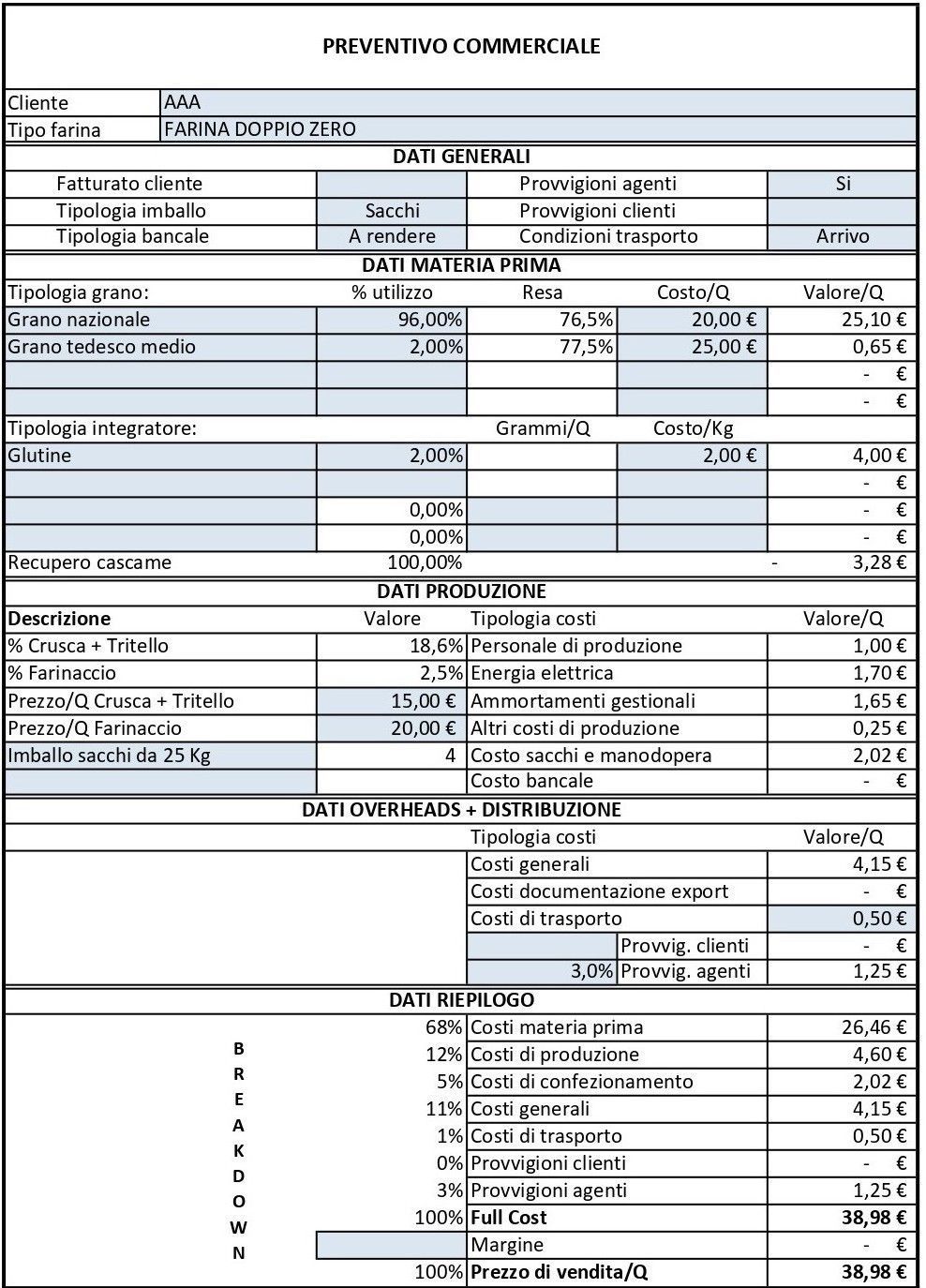

2) production of flour, upon specific customer request or for warehouse storage;

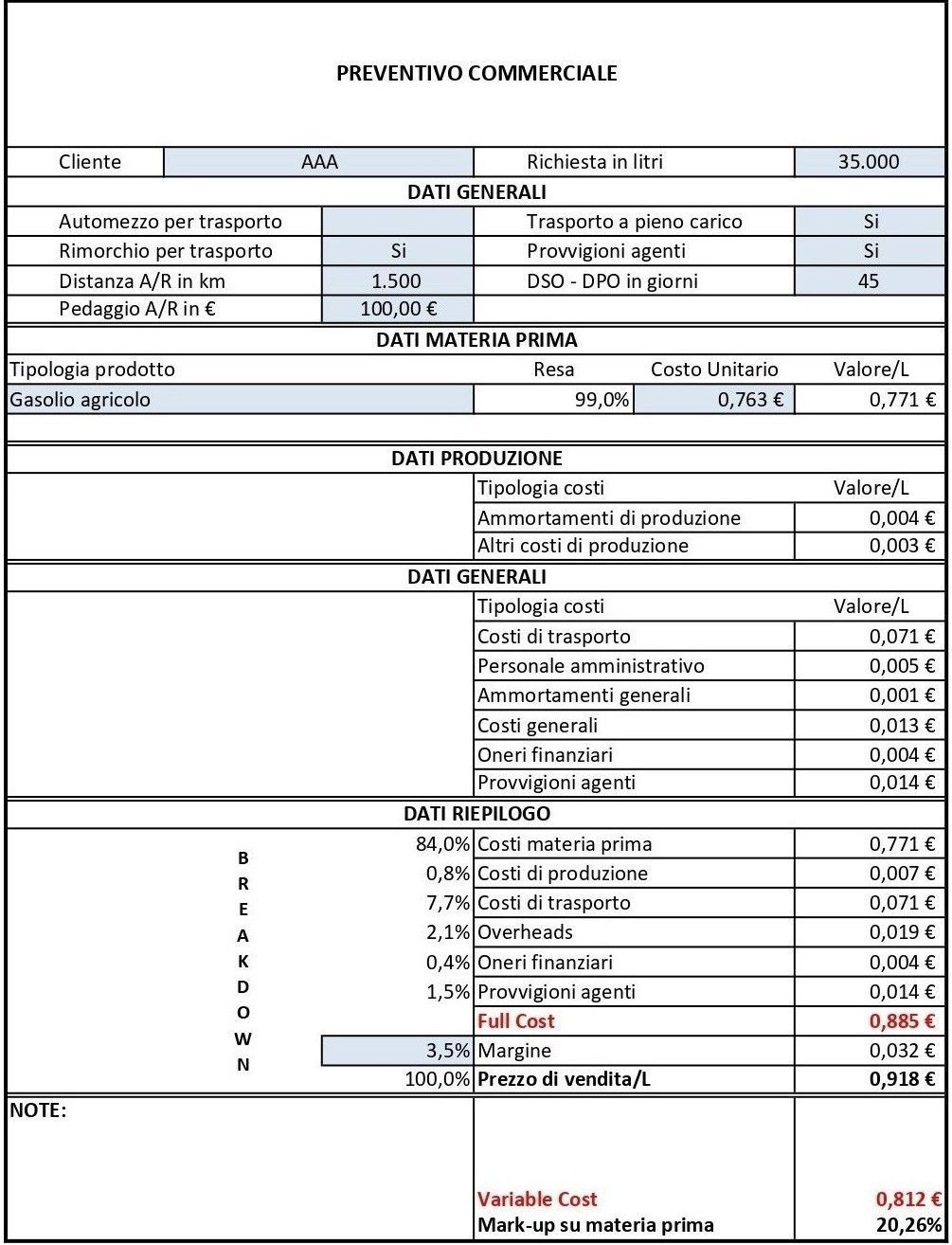

3) marketing of petroleum products.

1) In the technical articles moulding sector, the variables that influence the selling price are numerous and interconnected.

On one side, there's the raw material, with its specific characteristics—type, colorant, final application, minimum batches, inserts, and scraps—; on the other, the transformation phase, which includes mold washing, setup, press type, production method (automatic or manual), processing waste, kiln and packaging cycles, and even the type of packaging used.

All these elements, combined with the possibility of amortizing the cost of the mold directly on the product, make the estimate template extremely detailed and precise, providing a solid basis for correctly determining the selling price and protecting company margins.

2) In the milling sector, the variables to consider are numerous and closely linked to each other.

The different types of purchased wheat are transformed into flours for food use, each with specific characteristics determined by the processing "recipes" and the supplements added during the production process.

This processing also produces by-products such as bran and bran meal, which are used in the livestock sector as feed for livestock.

The differences in production formulas, combined with the packaging and transportation methods of the finished product, allow us to develop a comprehensive calculation model, capable of considering every variable in determining the optimal selling price and correctly assessing profitability by product line.

3) In companies dealing with the purchase and sale of petroleum products, the apparent simplicity of the business - devoid of a real transformation process - is only partial.

Behind the purchase and resale of raw materials lies a significant logistical complexity, linked to the loads transported, the distances traveled, and the delivery conditions.

It is precisely these factors that determine the difference between a profitable operation and a losing one.

Our quote template allows for the precise calculation of these variables, offering entrepreneurs a precise estimate of logistics costs and, consequently, a true assessment of the profitability of each transaction.